- The break-even point is the point at which zero profit is achieved.

- Before calculating your breakeven point, you need to know your costs

Did you know that the “break-even point” is an indicator of the soundness of a business and the financial condition of a company? This figure, which measures the balance between costs, sales, and profits, not only represents the current business situation but is also important to understand in order to know the health of a company, such as whether or not there is a need for improvement.

Key Takeaways

- Did you know that the “break-even point” is an indicator of the soundness of a business and the financial condition of a company?

- Understanding calculate the break-even point helps businesses make informed financial decisions and stay compliant.

- When calculating the break-even point, it is very important to consider “costs.” Costs can be broadly divided into the following two categories.

The break-even point is the point at which zero profit is achieved.

The break-even point refers to the point at which zero profits are achieved, a situation where there are no operating losses but no profits. In other words, it is the calculation of the amount where sales = expenses.

Regardless of the industry, businesses incur various costs to create goods and services and make profits by selling them. There is hardly any business with zero costs. Regardless of the size of the business, there must be some expenses that are incurred before profits are made.

If the break-even point is exceeded, the business will fall into the red and management will become difficult.

However, if the minimum break-even sales can be secured every month, it is possible to maintain the status quo, although it will not be profitable.

However, this does not allow any improvement activities to increase sales. This is because the costs to be invested there cannot be raised.

Businesses must always secure a minimum profit. Therefore, understanding the break-even point is essential.

Before calculating your breakeven point, you need to know your costs

When calculating the break-even point, it is very important to consider “costs.” Costs can be broadly divided into the following two categories.

- Fixed costs

- Variable costs

By considering each cost separately, you can analyze the cost structure of a company or business in more detail. We will explain in detail what each cost is.

Fixed costs

Fixed costs are costs that occur regardless of sales. For example, office rent, labor costs, various insurance premiums, interest on loans, and property taxes on real estate owned by the company are all fixed costs. These costs are always fixed regardless of sales increases or decreases, so the amount does not fluctuate from month to month.

Labor costs, etc., may fluctuate from month to month due to salary increases or an increase or decrease in part-time employees. Each company may consider the salaries of part-time employees and temporary employees to be variable costs, so be flexible in your response.

Variable costs

Variable costs are expenses that increase or decrease depending on sales . In the retail industry, this would be product purchasing, and in the manufacturing industry, this would be material costs and processing costs. The more products you sell and the higher your sales, the higher the cost will tend to increase.

Other variable costs include utility bills, shipping payments, and sales commissions. Keep this in mind as it is important to consider your break-even point.

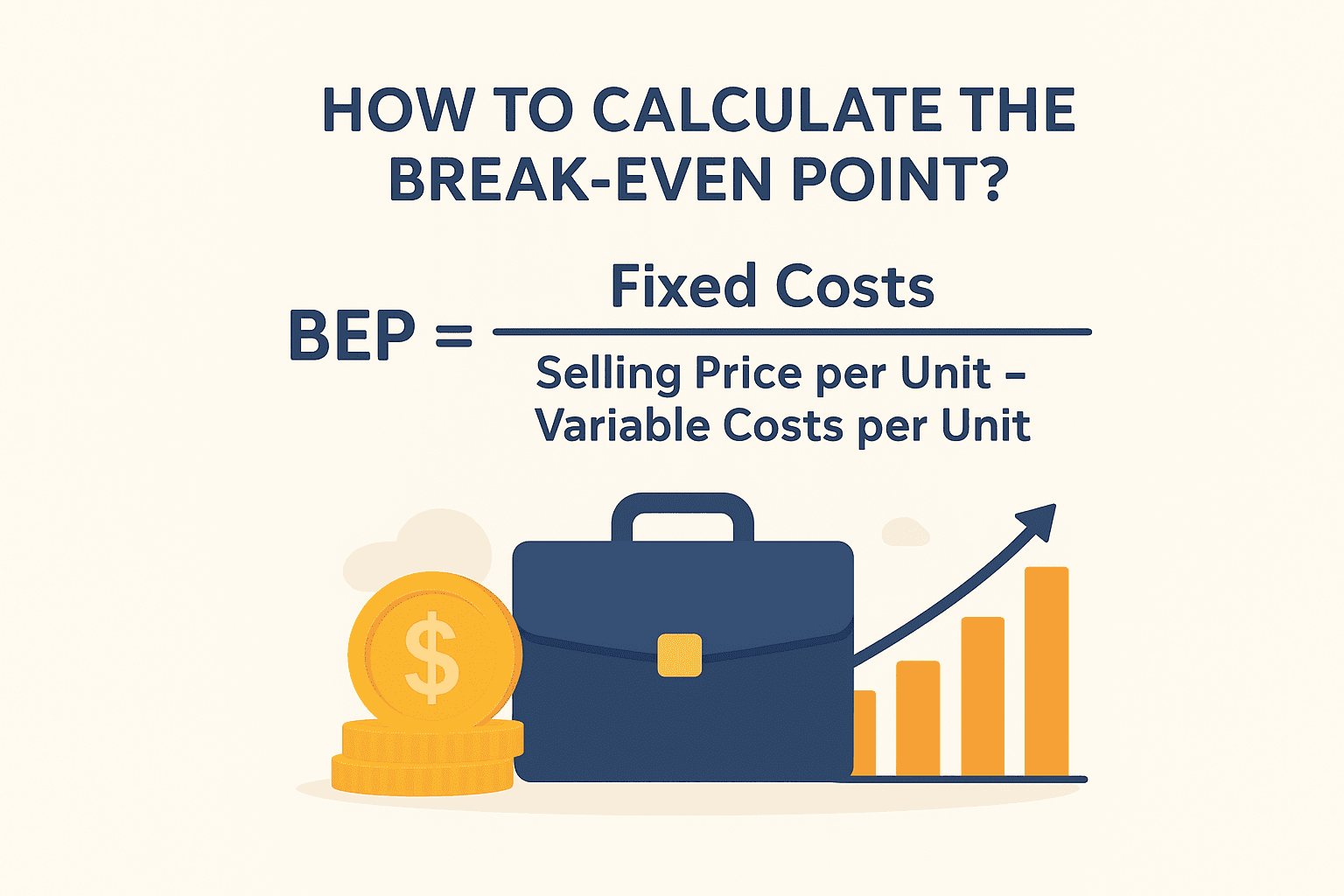

Formula and steps to calculate breakeven point

To calculate the breakeven point, you first need to remember the steps in the formula.

- ・Break-even point calculation formula

- ・Example of break-even point calculation

Let’s explain these two and learn how to calculate them.

Break-even point calculation formula

There are two ways to calculate the breakeven point.

- ①Break-even point = fixed costs ÷ {1 – (variable costs ÷ sales)}

- ②Break-even point = fixed costs ÷ (1 – fluctuation rate)

The part in formula ①, {1-(variable costs ÷ sales)}, is called the marginal profit ratio, and the break-even point can be calculated from two main factors: “fixed costs” and “marginal profit ratio.” Formula ② is a simplified version of formula ①.

Break-even point calculation example

Once you know how to calculate, it’s time to actually do the calculations. As an example, let’s assume a company has sales of $20 million, variable costs of $8 million, and fixed costs of $10 million. After subtracting costs from sales, the profit is $2 million.

Although the company is not in the red, the profit margin is only 10%, which is not high. Let’s calculate these figures using the following formula.

Formula①Fixedcosts ÷ {(sales – variable costs) ÷ sales} = break-even pointSales $10 million ÷ {($20 million – $8 million) ÷ $20 million} = $16,666… million

In the case of this company, if variable costs and fixed costs remain the same, the break-even sales amount will be $16.66 million. You can simplify the formula even more.

Formula ②Fixed costs ÷ (1 – variable cost rate) = break-even point Sales 10 million ÷ (1 – 0.4) = $16,666… million

The variable cost rate represents the ratio of variable costs to sales. You can calculate it using the formula “variable costs ÷ sales.” In this example, the variable cost rate is “8 million ÷ 20 million = 0.4.” By substituting into the formula, we confirm the value matches formula ①.

What is the break-even ratio?

The break-even ratio is a key indicator of a company’s business condition. It compares the current sales amount to the break-even point. This ratio is expressed as the ratio between the sales amount and the break-even point.

Let’s calculate it using the example provided above.

Break-even point ÷ Sales x 100 = Break-even point ratio (%)

$16.66 million ÷ $20 million x 100 = 83.3 (%)

If sales are equal to the break-even point, profits are close to zero. The break-even ratio in this state is 100%, so the smaller the break-even ratio, the better .

Although what number is appropriate varies depending on the industry, a ratio below 70% is considered a good condition, in the 80s is roughly average, and 90% is considered a dangerous zone, so immediate action will be required. If it exceeds 100%, losses are already occurring, so action must be taken immediately.

What is the margin of safety?

The margin of safety is a rate that tells you how much your current sales are above the break-even point . It tells you how profitable your current business is. It is also a number that means that even if there are some phenomena within the margin of safety, you will not go into the red.

The method for calculating the margin of safety is as follows.

Formula:

Margin of Safety = (Sales – Break-Even Sales) ÷ Sales x 100

Let’s use the sales example we gave earlier to help us do the calculations.

(20 million – 16,666,000) ÷ 20 million x 100 = 16.7

In this case, it indicates that even if sales fall by another 16.7%, the company will not go into the red .

If the company or the business is in the red, the margin of safety will be a negative number.

What you can learn from the break-even point

If you know the concept and formula of the break-even point, especially the variable cost rate, you can easily calculate how much profits change with changes in sales, and how much sales are needed to achieve the target profit. By understanding the relationship between expenses, sales and profits, you will be able to take future management measures while considering various situations .

In addition, if you have knowledge of the break-even rate, you will be able to understand that the discounted amount is not just a discount, but also whether discounting may result in a loss. This knowledge is necessary not only for business representatives but also for sales representatives.

Summary of this article

The breakeven point is the point at which a business starts from zero profit.

・The break-even point occurs when zero profits are made. It is when the business is neither losing money nor making a profit.

Before calculating your breakeven point, you need to know your costs

- Fixed costs

- Variable costs

Formula and procedure for calculating breakeven point

・Break-even point calculation formula

・Example of break-even point calculation

What is the break-even ratio?

・The rate at which you can find out what your current sales figures are compared to the break-even point

What is the margin of safety?

・The rate at which you can know how much your current sales are above the break-even point

What you can learn from the break-even point

You can easily calculate how much profits will change with changes in sales, and how much sales are needed to achieve your target profits.

Related Articles: