- Debit and Credit: The Basics You Need to Know

- How are debit and credit different in accounting?

Debit and credit are fundamental to accounting systems used by companies. This system is based on double-entry bookkeeping. The basic mechanism is to carry out a procedure of recording accounting entries, which must result in the accounts being balanced at the end of the accounting entry.

Key Takeaways

- Debit and credit are fundamental to accounting systems used by companies.

- Understanding debit and credit isn’t just a matter of accounting theory: it’s an essential skill for effectively managing your business finances.

- In accounting, the mathematical symbols + or – are not used to record cash inflows and outflows.

Debit and Credit: The Basics You Need to Know

To simplify, think of your accounting as a notebook in which you write down everything that comes in and everything that goes out.

Every time you make a transaction (pay a bill, sell a product, collect a payment), you must record it in two places: a debit side and a credit side.

Why? Because in a business, every movement of money always has an origin and a destination.

Simple definitions

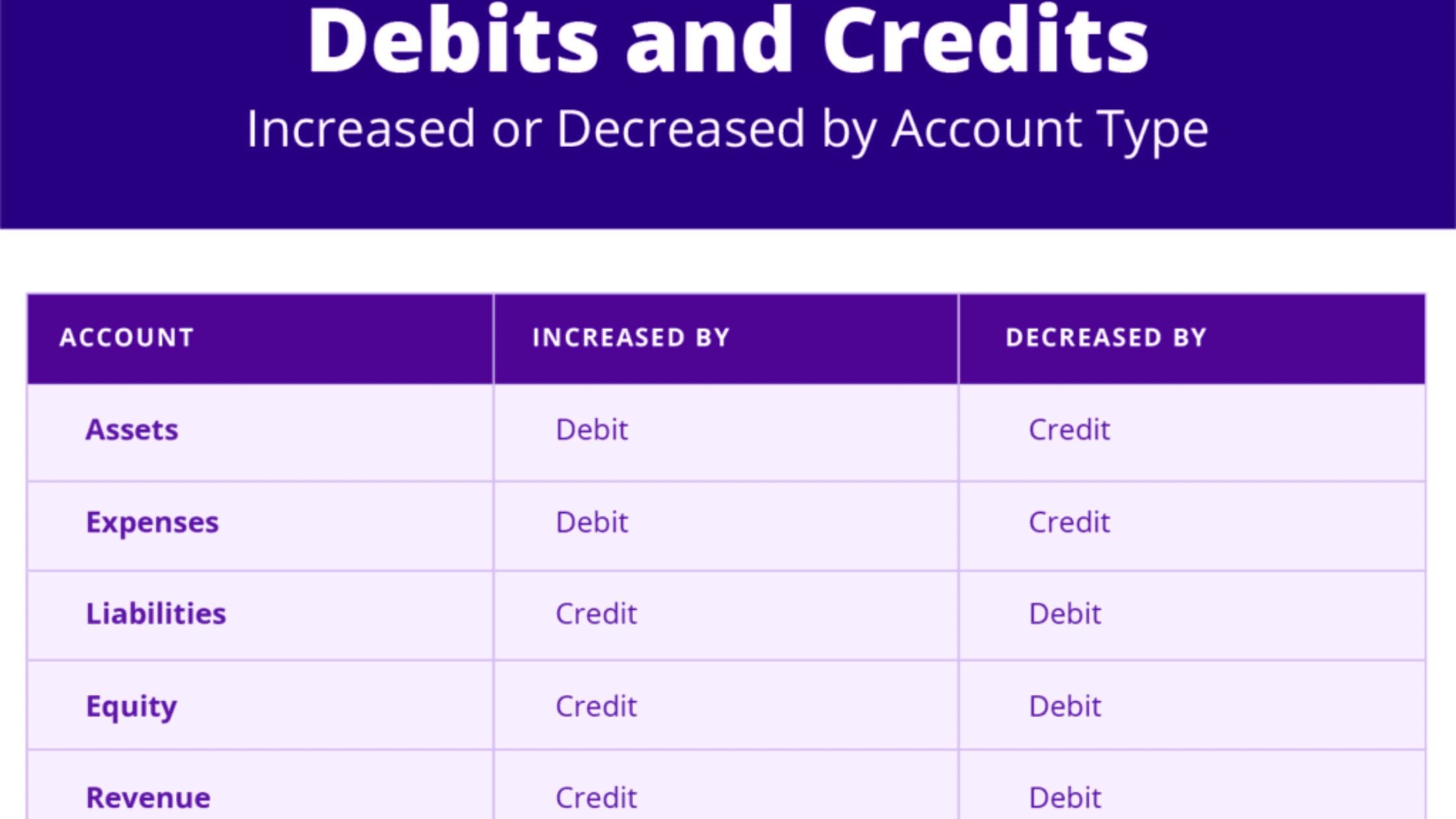

- Debit: What you receive or what increases in your assets (i.e. what you own).

- Credit: What you spend or what increases your liabilities (i.e., what you owe).

A simple rule: everything must balance.

In accounting, we use the double-entry method. This means that the same transaction is always recorded twice: once as a debit to one account, and once as a credit to another. And these two amounts must always be identical for your accounts to balance.

This system is essential for preparing essential financial documents, such as the balance sheet or income statement, which will help you analyze the overall financial health of your company and identify possible imbalances

Concrete examples to better understand

Example 1: You buy equipment for $500

1 – Debit: the “Purchase of equipment” account increases by $500 (you spent money to buy equipment).

2 – Credit: a decrease in the ‘Bank’ account (you have less funds).

These entries may also concern specific assets such as fixed assets (tangible or intangible).

Example 2: You sell a product for $1,000

1 – Debit: the “Bank” account increases by $1,000 (you receive money).

2 – Credit: the “ Turnover or sale of services” account increases by $1,000 (you record income).

By understanding these different points, you will be able to properly master and monitor your company’s accounting.

How are debit and credit different in accounting?

In accounting, the mathematical symbols + or – are not used to record cash inflows and outflows. This is mainly because companies keep accrual accounting, and therefore transactions may be recorded in the accounts but not be effective until later. Therefore, the terms debit and credit are used.

Concept of debit in accounting

The concept of debit in accounting records relates to transactions that third parties owe to the company. For a customer who owes money to the company and makes a payment, the transaction is recorded in the debit column of the account.

Concept of credit in accounting

As its name suggests, an account credit is the opposite of a debit. In accounting records, it refers to financial transactions that the company owes to third parties, such as supplier payments.

The importance of the concepts of debit and credit

Understanding debit and credit concepts can be counterintuitive. Yet, they are crucial for maintaining a company’s financial records. Debit and credit are complementary concepts.

In many countries, double-entry bookkeeping is required by the accounting system.

Debits and credits must always balance each other. Each transaction is recorded twice—once as a debit and once as a credit. Accounts are divided into two columns: debit on the left and credit on the right, following standard conventions.

How to record a debit and a credit?

The way to record a debit and a credit depends on the account being produced: the income statement and the balance sheet account.

Accounting entries in the income statement

An income statement consists of income and expenses.

Expenses represent the costs that reduce a company’s bottom line.”. You should record raw material purchases, supplies and equipment purchases, and personnel costs as debits.

Revenue represents the income generated by a business. Therefore, sales and grants received must be recorded as debits.

Accounting entries in the balance sheet account

The balance sheet account consists of assets and liabilities.

Assets represent what the company owns. Therefore, anything that increases assets should be debited, such as a customer’s receivable, inventory, investments, etc. Conversely, anything that decreases assets should be credited, such as the settlement of a customer’s receivable.

Liabilities represent what the company owes. Anything that increases liabilities should be recorded as a credit, such as a debt to a supplier, provisions, reserves, etc. Conversely, anything that decreases liabilities should be recorded as a debit, such as the settlement of a debt to a supplier.

Why is this important for your business?

Understanding debit and credit isn’t just a matter of accounting theory: it’s an essential skill for effectively managing your business finances.

These concepts directly affect the accuracy of your accounts and the financial health of your business. Here’s why:

1 – Track your finances accurately

Debit and credit allow you to understand exactly where your money is coming from and where it’s going. This gives you a clear view of your business.

2 – Prepare your financial statements

These records are used to produce essential documents such as the balance sheet or the income statement, essential for analyzing the health of your business.

3 – Avoid financial mistakes

Careful monitoring allows you to detect inconsistencies and keep your accounts balanced.

If you have any doubts, it is often useful to seek the support of a trustee, particularly if you have just started your business.

Conclusion

Debit and credit may seem intimidating at first, but they’re simply two ways to track every movement of money in your business. Remember, every transaction is double-sided: what goes in one side goes out the other.

With a little practice, these concepts will become second nature, allowing you to manage your finances with complete peace of mind.

FAQs

What is debit in accounting?

The concept of debit in accounting records concerns transactions that third parties owe to the company. For a customer who owes money to the company and makes a payment, the transaction is entered in the debit column of the account.

How not to get confused between debit and credit?

To verify the accuracy of your accounting records, you must compare the total debits and credits. These totals must be exactly equal. This is the rule of double-entry bookkeeping.

Related resources: Learn about general ledger basics and explore the different types of accounting.